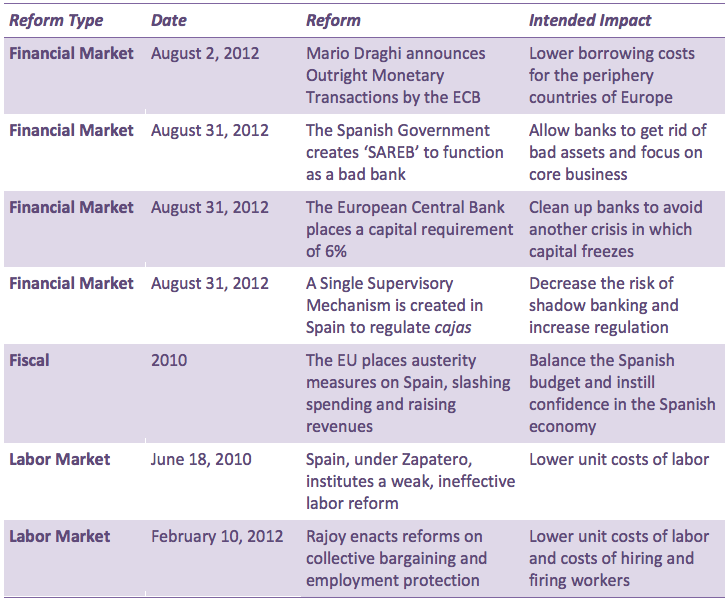

Featured Article:The Spanish Financial Crisis: Economic Reforms and the Export-Led RecoveryEconomic ReformsBy 2008, the Spanish government was borrowing at a rate of nearly 5%,20 and businesses were hard pressed to find financing at any rate. The future of Spain was uncertain as investors and business owners questioned whether Spain would stay in the Eurozone. Hiring and credit markets froze; unemployment rose to 20% in 2010 from 8% in 200821 and loans over €1 million to companies dropped 25% from 2009 to 201022, as companies awaited a response from the Spanish government. Yet, then Prime Minister José Luis Rodríguez Zapatero was slow to institute any significant reforms. The socialist leader had political pressure from the left to uphold government services and labor-friendly labor laws. In 2011 Mariano Rajoy was elected as a more conservative candidate from the People's Party, as voters showed their frustration with Zapatero's response to the crisis. With an absolute majority in the legislature with 186 of 350 seats, Rajoy immediately began implementing reforms to address the issues.23 The reforms that the Rajoy government enacted in response to the crisis, highlighted in Table 1, can be placed into three main categories: financial market reforms, fiscal measures and labor market reforms. Each reform was put into place to stabilize the macroeconomy of Spain and to allow for the return to capital markets for both the government and businesses. The Spanish economy needed a renewed sense of credibility within global markets, and the reform effort was aimed at reinstating this credibility to put Spain on the road to recovery.Table 1: Spanish Economic Reforms, 2010 - 2012

Financial Market ReformsTo restore confidence in the periphery: countries like Spain, Portugal, Ireland and Greece outside the core of Europe, on August 2, 2012 the European Central Bank's president Mario Draghi announced that the ECB was prepared to undertake Outright Monetary Transactions (OMT) to aid ailing countries, and that Spain would be granted up to €100 billion to salvage its banking system.24 The ECB recognized that the system that had allowed for the origination of millions of mortgages in Spain, many of which were to subprime borrowers with little equity to back up the loans, needed to be changed. In exchange for the ECB's pledge of support, Spain was required to administer certain reforms in its financial system. First, on August 31, 2012, with the Spanish Royal Decree-Law 24/2012, the Spanish Government created SAREB (Sociedad de Gestión de Activos procedentes de la Reestructuración Bancaria) that functioned as a typical 'bad bank.'25 €40 billion worth of assets were transferred from four of Spain's previously nationalized financial institutions: BFA:Bankia, Catalunya Banc, NGC Banco-Banco Gallego and Banco de Valencia. These assets consisted of bad loans from the mortgage crisis and allowed the original institutions to focus on their business while a new entity could focus solely on the restructuring and sale of the bad assets. The government branch, the Fund for Orderly Bank Restructuring, owns 45% of SAREB while private shareholders hold the other 55%. The bank has 15 years to dispose of the assets and aims to make a 15% cumulative profit.26 The next task was to better capitalize Spain's functioning banks. Many banks, with low amounts of capital in the first place, had yet to write off all of the underperforming loans due to the housing crisis. In order to avoid another crisis of the same scale, and instill confidence in the banking system, the European Union ordered banks to raise their capital levels in line with the European Central Bank stress tests of 6% of assets.27 Banks receiving state aid were required to shed their riskiest assets to comply with risk-weighted capital requirements. Finally, Spain set out to rein in the largely unregulated 'caja' system that had been in place for hundreds of years. Spain instituted a reform of the framework for regulation, allowing for a Single Supervisory Mechanism over the banking system and enhancing the Banco de España's regulatory and supervisory powers, granting them sanctioning and licensing power. The reforms required that the cajas have formal shareholders with a system to distribute profits, and attempted to centralize the regulatory authorities in order to place the same requirements on all banks and reduce the risk of shadow banking that helped lead to the housing bubble of 2008.28 Each of these reforms attempted to restore the banks' access to funding markets, to allow for banks to start lending to businesses once more and, eventually, to propel the economy forward. Fiscal MeasuresIn the aftermath of the crisis, the Spanish budget immediately saw a disproportionate decrease in revenues rather than a significant increase in expenditures. The Spanish government increased its expenditures by a cumulative 6% of GDP from 2007 to 2011, which was in line with the rest of the Eurozone; in fact, its level of expenditure in 2011 (45% of GDP) was below the Eurozone average of 50% of GDP. Revenues, on the other hand, decreased 5.4% of GDP from 2007 to 2011, more than any other country in the Eurozone. Further, Spanish revenues were only 36% of GDP in 2011, compared to the Eurozone average of 45% of GDP. The problem of revenues was a direct consequence of the housing crisis in Spain; many of the taxes collected in the period before the crisis were temporary taxes linked to the transfer of property. Additionally, as unemployment rose, Spanish income tax revenues decreased.29 To combat the fiscal problems, Spain has gone through two distinct phases: an expansive phase from 2008-2009 and a consolidation phase from 2010 to the present day. Both phases came at the recommendation of the European Union, and have produced significant effects on the fiscal situation of Spain. During the expansive phase, Spain merely added to its budgetary problems. It instituted tax cuts totaling 1.8% of GDP in 2008 and 2009 and introduced liquidity support to households and companies that reduced revenues by an additional 1.2% of GDP. Further, the governments introduced a fund for local public investment and a fund to aid strategic sectors which added an additional 1.1% of GDP to expenditures. Due to these policies, Spain shifted from a budget surplus of 2% in 2007 to a deficit of 11% in 2009, and public debt increased from 36% to 54% of GDP from 2007 to 2009.30 The consolidation phase came as the European Union realized the need for the periphery of Europe to shore up its accounts in order to raise public debt at affordable levels, and the EU placed austerity measures on Spain. The government instituted revenue measures with an expected positive impact of 3.9% of GDP by raising the value added tax rate from 21% to 18% and significant income-tax increases. Additionally, the government laid out expenditure measures with an expected reduction of 3.5% of GDP, most notably, cutting jobless benefits and public-sector wages by 7% and reducing departmental budgets by 17%.31 32 Another important aspect of Spain's fiscal landscape is the presence of autonomous regions, roughly equivalent to states in the United States. The regions, through health care, education and social services, outlay 35% of total government expenditures in Spain, yet bring in only 19% of total revenues in taxes. The deficits are filled in by transfers from the central government, contributing to 56% of the deficit in 2009. Currently, reforms are being made by the central government to ensure that the regions practice fiscal responsibility and to more properly allocate capital to regions to reflect the proper use of government resources. Additionally, Rajoy is implementing a system by which the central government can place austerity measures on the regions in exchange for financing, similar to Europe's treatment of Spanish finances. This would force regions to start raising personal-income taxes and decrease spending on public services. 33 Specifically, the government is requiring that the regions aggregately raise revenue and decrease expenditures by €4 billion in both 2014 and 2015.34 Labor Market ReformsAs domestic demand in Spain decreased due to the housing crisis and subsequent employment crisis, Spain needed to become more competitive in the global market place. Most countries would use their central banks to lower interest rates and devalue their currencies, yet this option was not available to Spain because of its participation in the Eurozone. The other option to increase competitiveness globally was to decrease unit labor costs, which would in turn allow Spanish exporters to reduce their prices. Spain was renowned for its archaic labor laws, as companies found it difficult to fire employees, employees enjoyed early retirement with full pensions, powerful collective bargaining positions, and, most importantly, constant wage increases. While its GDP (-7%) and employment (from 9% to 20% unemployment) levels fell precipitously in the three years beginning in 2008, Spain's unit labor costs actually increased by an average of 1.7% a year.35 Spain began to address these issues with a labor reform in 2010, but it wasn't until February 10, 2012 with the Royal Decree Law 3/201236, that Rajoy was able to enact a monumental labor reform. The 2012 labor reform consisted of two main initiatives: reforming the collective bargaining aspect of Spanish labor and adjusting the employment protection legislation. The reforms attempted to hit the heart of the matter; Spain needed to reduce its labor costs and had to wrest power from its employees. The first step was to give priority to collective bargaining agreements (CBA) at the firm level over those established at the sector or regional levels. This allowed for Spanish firms to become more competitive amongst each other, and made it easier to decrease wages without strikes. The new CBA reforms allowed for firms to opt out of an agreement and implement "internal flexibility," meaning firms could introduce unilateral working condition changes for economic or productivity reasons. For example, Spanish firms were now able to change the wages and working hours of employees in order to increase profits, a practice that was unheard of before 2012. In addition, in the absence of an agreement of internal flexibility, an employer could refer the matter to a relatively speedy arbitration rather than go through a full review by labor courts, allowing changes to a company's workforce to go through more quickly without high costs for litigation. The employment protection legislation, specifically relating to regulations on hiring and firing, was also made more business friendly. The definition of fair economic dismissal was reshaped to mean that dismissal is always justified if a company faces three quarters of decline in revenues or income. In other words, companies no longer had to prove that dismissals were essential for future profitability. The reforms also reduced monetary compensations for dismissal and eliminated the requirement of administrative authorization for collective redundancies. Traditionally in Spain, in order to lay-off a large amount of workers, companies had to obtain government approval, and government approval was sometimes denied if the company could not agree with the union board about the layoffs. Now that government approval was no longer necessary, companies could perform massive layoffs without consulting union boards.37 Finally, the law instituted "contrato emprendedores," which allowed firms under 50 employees to have a one year trial period for full-time employees, attempting to spur hiring by entrepreneurs.38 The new labor reforms modified a labor system that was strongly rooted in the 'uncertainty avoidance' of Spanish culture discussed in the introduction of this thesis, with many protections for workers. With a gloomy outlook on the future of domestic demand due to the high unemployment and debt levels, and the lack of ability to institute monetary policy, Spain saw labor reform as the best way to increase its global competitiveness.Continued on Next Page »

KEYWORDS:

From the Inquiries Journal Blog ")  Monthly Newsletter SignupThe newsletter highlights recent selections from the journal and useful tips from our blog. Suggested Reading from Inquiries Journal

Inquiries Journal provides undergraduate and graduate students around the world a platform for the wide dissemination of academic work over a range of core disciplines. Representing the work of students from hundreds of institutions around the globe, Inquiries Journal's large database of academic articles is completely free. Learn more | Blog | Submit Follow IJ

Latest in Economics |