Featured Article:Capital Controls in Emerging Market Economies: Comparing Their Use and Effectiveness in Five CountriesThailandThailand has a long history of using capital controls and this study will examine two specific time periods when the country used these controls on outflows and inflows, respectively: starting in March 1997 and again beginning in 2006. Evidence from various studies has shown that these capital account restrictions were not ultimately effective; these controls were unable to prevent Thailand’s currency crisis in the 1990s and exchange rate volatility in the mid-2000s. However, the country’s control on capital outflows in 1997 proved to be more damaging than its controls on capital inflows in 2006, as the former contributed to the country’s currency crisis while the latter was ineffective but not harmful.

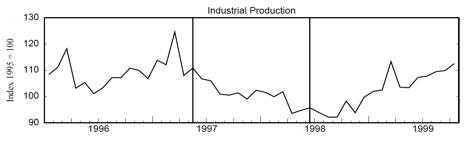

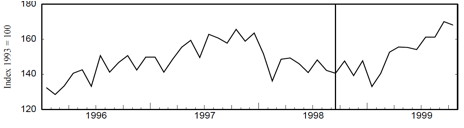

Figure 3.1 - Thailand’s Industrial Production, 1995=100 (Edison and Reinhart 2000, 33)

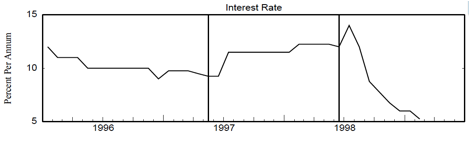

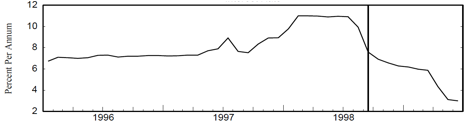

Figure 3.2 - Thailand’s Interest Rate (Edison and Reinhart 2000, 33)

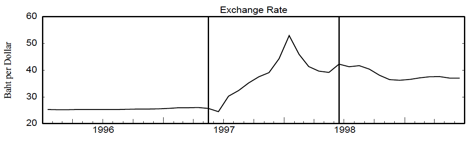

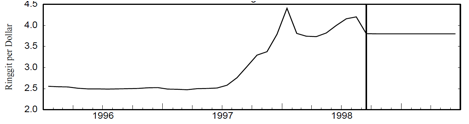

Figure 3.3 - Thailand’s Exchange Rate (Edison and Reinhart 2000, 33)

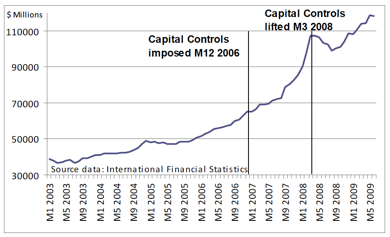

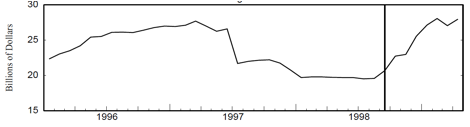

Figure 3.4 - Thailand’s Foreign Reserves, 2003-2009 (Coelho and Gallagher 2010, 10)

Thailand has historically used extensive capital controls for years prior to 1990, which allowed the country to maintain a degree of monetary independence even though it had a fixed exchange rate (Warr, 1999, p. 634). However, in the late 1990s, Thailand experienced a severe currency crisis that many policymakers believe was exacerbated by the country’s use of capital controls (Edison and Reinhart, 2000, p. 11). The reason Thailand had implemented these controls in the first place is because the country’s capital stock started growing significantly starting in 1987. While both foreign direct investment (FDI) and domestic investment contributed to this increase in capital flows, the growth in FDI was considerably larger than the growth in domestic investment (Warr, 1999, p. 632). The capital control measures focused on stemming outflows that Thailand implemented during the 1990s tried to close speculation channels by preventing speculators from accessing funds. However, the controls did not prove to be effective in averting capital outflows, as outflows started increasing from May 1997 onwards even though the controls were in place. Moreover, as a result of these controls, Thailand experienced a wide range of adverse effects: the country’s industrial output decreased (see Figure 3.1), its foreign exchange reserves declined, its interest rates increased (see Figure 3.2), and its exchange rate became more variable and devalued significantly against the U.S. dollar (see Figure 3.3). More specifically, while the volatility of Thailand’s interest rates decreased during the time the country implemented controls, the interest rate level still increased. (Edison and Reinhart, 2000, p. 9, 12 and 15). The graphs in the neighboring figures demonstrate the changes in these economic indicators—for industrial output, foreign exchange reserves, interest rates, and exchange rate—at the times when Thailand imposed and raised its controls, which occurred in 1997 and 1998, respectively. These results indicate that Thailand’s capital controls did not insulate its economy and prevent a currency crisis as it had hoped to do. In 2006, the Thai baht was experiencing considerable appreciation, so the Bank of Thailand (BOT) decided to interfere in the capital market. However, the BOT’s capital market interventions did not prevent the baht from continuing to rise as foreign reserves continued to grow (see Figure 3.4), so the BOT implemented controls to decrease capital inflows and it decided to reverse capital account liberalization measures beginning in December 2006. More specifically, the BOT banned financial institutions from participating in certain foreign exchange market activities, such as issuing and selling exchange earnings, in order to curb speculation and forbade the sale or purchase of debt securities. Since the Thai baht continued to appreciate, the BOT then decided to impose a 30 percent URR on most categories of capital inflows, with the exception of FDI and when amounts were less than $20,000. Beginning in 2007, Thailand’s capital control measures were altered and other types of transactions were included in the exclusions from the URR. When credit began to constrict in the early months of 2008, the Thai baht was no longer under appreciation pressures and first the BOT raised several of its limits on capital account transactions and eventually removed the URR completely (Coelho and Gallagher, 2010, p. 10-11). Thailand’s 2006-2008 capital controls had varying degrees of effectiveness depending on the economic measures being assessed. While Thailand’s URR did manage to diminish the overall volume of capital flows—by approximately 0.75 percent of GDP—and the initial announcement of the control measures resulted in a decline in asset prices, the controls still resulted in increased exchange rate volatility and asset prices returned to their upward trend immediately following the URR announcement (Coelho and Gallagher, 2010, p. 1 and 16). Accordingly, it is apparent that Thailand’s controls in the mid-2000s were effective to a certain extent and ineffective at their worst, but they were not as harmful as the controls on capital outflows that the country had implemented in the late 1990s. MalaysiaWhile the capital controls imposed by Malaysia in 1998 received significant global attention, the country has actually had controls in place since 1953 (Cooper, Tarullo, and Williamson, 1999, p. 118). The primary reason why the 1998 controls were thrust into the spotlight is because Malaysia’s response to the Asian financial crisis was markedly different from how the other affected countries reacted. When the Thai baht devalued substantially in July 1997, many Southeast Asian countries experienced massive capital outflows that resulted in lower local equity prices and declining exchange rates. As a result, the IMF encouraged these nations to raise their interest rates in order to attract foreign investors to their securities; however, these higher interest rates caused slower growth in the countries’ domestic economies (Edison and Reinhart, 2000, p. 9-10; Neely, 1999, p. 22). Rather than turn to the IMF for guidance, Malaysia decided to tackle these issues on its own by instituting a series of capital controls in September 1998 (Abdelal and Alfaro, 2003, p. 37). The Malaysian controls were mainly aimed at preventing capital outflows, as they prohibited transfers between domestic and foreign accounts as well as between different foreign accounts, lifted credit amenities to foreign investors, delayed returns on investment for a year, and fixed the exchange rate. Moreover, foreign exchange transfers were limited to being done for current account reasons at specific institutions that the government identified and the Malaysian government instituted regulations to prevent evasion of its controls. These controls were altered slightly in February 1999 when the government decided to replace the ban on returning capital with taxes on outflows instead. Overall, the Malaysian government instituted these capital controls in an effort to discourage capital flows in the short-term but allow longer-term transactions to continue unimpeded and it hoped to be able to retain a greater level of monetary independence in the process (Johnson, et al., 2007, p. 533-534; Neely, 1999, p. 22). Figure 4.1 - Malaysia’s Industrial Production, 1993=100 (Edison and Reinhart 2000, 31)

Figure 4.2 - Malaysia’s Foreign Reserves (Edison and Reinhart 2000, 31)

Figure 4.3 - Malaysia’s Interest Rate (Edison and Reinhart 2000, 31)

Figure 4.4 - Malaysia’s Exchange Rate (Edison and Reinhart 2000, 31)

Evidence on the effectiveness of the capital controls reveals mixed and ambiguous results, on the whole. While the controls appear to have substantially reduced total capital flows, they were not successful in changing the composition of these flows. As a result, it appears as though the controls were able to help Malaysia attain monetary independence as it had hoped (Goh, 2005, p. 1493). The controls were also expected to have an impact on Malaysian industrial production, foreign exchange reserves, interest rates, and the exchange rate, each of which will be explored in turn. Immediately after the controls were imposed, industrial production declined considerably, but from September 1998 through 1999, industrial production increased by over eight percent (see Figure 4.1). Additionally, foreign exchange reserves in Malaysia grew $7 billion to $27 billion between late August 1998 and April 1999 (see Figure 4.2). Interest rates, on the other hand, declined to pre-crisis levels by 2000 after dropping from more than seven percent in 1997 to slightly more than three percent in June 1999 (see Figure 4.3). Finally, the exchange rate was stabilized when it was pegged against the dollar (see Figure 4.4), as the authorities had hoped would happen (Edison and Reinhart, 2000, p. 11). The graphs in the appendix depict the point in time when the Malaysian capital controls were implemented in 1998 and the trends in the macroeconomic indicators before and after the controls were instituted are apparent through an analysis of these graphs. Therefore, it is evident that Malaysia’s capital controls was not disastrous for the country’s economic performance in the short-run as many people had expected (Edison and Reinhart, 2000, p. 11). In fact, the country’s economy recovered soon after it instituted the controls, with GDP growth at 6.1 percent in 1999 and 8.2 percent in 2000 after it had declined by 7.4 percent in 1998. It is important to note, however, that this economic rebound still cannot clearly be attributed to Malaysia’s use of capital controls since there were other changes occurring simultaneously that could have contributed to the country’s recovery. First, the Malaysian ringgit depreciated by over 50 percent in the years of the Asian financial crisis, which allowed the country’s exports to become more competitive in the global market and Malaysia was able to capitalize on the strongly growing U.S. economy to which it exported large quantities of manufactured goods. Additionally, the U.S. Federal Reserve Chairman Alan Greenspan decided to lower interest rates in October 1998, which helped Asia recover from the various country crises it was facing (Abdelal and Alfaro, 2003, p. 39; Doraisami, 2004, p. 243; Jomo, 2002, p. 133-134). Furthermore, since Malaysia’s capital controls were actually imposed over a year after the financial crisis had begun in July 1997, it is likely that most of the investors who panicked and wished to withdraw their capital had already done so by the time Malaysia’s controls went into effect ((Abdelal and Alfaro, 2003, p. 39; Johnson et al., 2007, p. 558). Finally, it has also been argued that Malaysia’s economic recovery was not due to its imposition of controls, but rather, its pegged exchange rate (Edison and Reinhart, 2000, p. 11; Edwards, 2007, p. 4). Several negative effects of the Malaysian capital controls can also be identified. First, it is difficult to determine the extent of the administrative burden and costs that were associated with enforcing and complying with the controls (Doraisami, 2004, p. 252; Goh, 2005, p. 1501). In addition, the closure of the offshore market caused a reduction in investor opportunities, which would have resulted in economic losses that cannot be quantified. Furthermore, Malaysia’s imposition of capital controls led to the credit rating downgrade of Malaysia’s credit and sovereign debt ratings by international rating agencies and the increase in its country risk levels (Doraisami, 2004, p. 253). Finally, some studies have found that the controls did not only diminish short-term capital flows, but they may have also caused a decrease in long-term capital flows (Goh, 2005, p. 1501). Malaysia is often touted as an example of when capital controls are effective in the shorter-term as the country was able to use them in the interim as it planned the crucial reforms it would need to implement (Neely, 1999, p. 22). Proponents of Malaysia’s use of capital controls point to the increased stability of the country’s interest rates and exchange rates and expansion of its monetary autonomy as proof of the controls’ success. However, while the effects of the Malaysian capital controls suggest that they might have had a role in insulating the country’s economy from further economic damage, it cannot be said for certain that the controls were responsible for an improvement in economic performance. Other Southeast Asian countries—specifically South Korea and Thailand—that had been impacted by the crisis and did not institute controls were also able to enjoy similar interest rate and economic benefits as Malaysia (Edison and Reinhart 2000, 11 and 20). Some economists have argued that Malaysia’s recovery from the Asian financial crisis was actually the result of the country’s responsible macroeconomic policies, financial- and corporate-sector reforms, strong initial conditions, and institutional potential rather than the controls it had imposed (Johnson et al., 2007, p. 540). As a result, it is unclear whether the Malaysian capital controls can be credited for improving Malaysia’s economic situation (Jomo, 2002, p. 131). IndiaAnalyses of India’s use of capital controls during the 1990s have had varying results in terms of recommendations for whether India should implement widespread capital account liberalization or make it more selective. Proponents of India’s capital controls have argued that the use of these capital account restrictions can explain India’s stability during the East Asian crisis (Joshi, 2001, p. 305). However, supporters of capital account liberalization argue that only when India’s capital controls were loosened was the country able to achieve significant economic growth and development, as India’s capital controls were undoubtedly responsible for its previously low economic growth rate (Corden, 2002, p. 222). The case of India is not as clear-cut as many other countries that have used capital controls because India’s selective use of these measures appears to have been effective for certain narrow, short-term goals and the country has been careful to adapt its use of controls to the macroeconomic conditions present over the years. However, the fact that India’s controls are comprehensive and almost permanent has resulted in significant costs to the country’s financial system (Patnaik and Shah, 2012). The reason that India implemented capital controls in the 1990s is because from 1993 to 1995, it experienced a heavy influx of private capital flows that resulted from lower U.S. interest rates and the potential for profit raised by India’s reforms to its financial system. Moreover, India’s relatively high domestic interest rates along with its weaker fiscal and monetary policy caused many Indian firms to turn to foreign investors in order to raise capital (see Figure 5.1). As a result of these changes in capital flows—particularly inflows—Indian policymakers needed to determine how to establish the country’s macroeconomic policy, especially its exchange rate policy (Corden, 2002, p. 221; Joshi, 2001, p. 308). Figure 5.1 - Net Capital Inflow to India, 1985-1999, Percent of GDP (Athukorala and Rajapatirana 2003, 618)

Prior to 1991, capital controls in India were implemented on a case-by-case basis and they were constricting enough to significantly reduce FDI. Beginning in 1992, an automatic approval of up to 51 percent shareholding of FDI was allowed for various industries; since 1996, foreign equity of up to 74 percent in a wider range of industries have allowed FDI. With respect to foreign portfolio investments, before 1991, India did not allow these types of investments, but beginning in 1992, foreign institutional investors were given permission to invest in listed securities such as equities and bonds in India. Furthermore, starting in 1997, foreign institutional investors were allowed to invest in government securities and treasury bills in India (Joshi, 2001, p. 306). As this progression of events depicts, India’s system of capital controls started to be selectively liberalized—especially with respect to direct and portfolio inflows—in the 1990s (Joshi, 2001, p. 307). As a result, even though it appears as though capital controls did have a role in helping India maintain exchange rate stability and monetary autonomy in the face of the East Asian crisis in the 1990s (Joshi, 2001, p. 317), these controls still had negative side effects on the country’s economy and caused the bureaucracy and private firms to experience administrative costs (Corden, 2002, p. 222). The three types of costs associated with India’s use of capital controls include the following: the costs derived from driving a wedge between foreign and domestic capital markets, the higher domestic cost of capital, and governance-related costs. The price differences between foreign and domestic markets has caused India to pay a higher cost of capital and the controls have also caused unintended microeconomic distortions for the country. For example, when India introduced a rule in August 2007 that only permitted foreign borrowing for importing capital goods, there was a consequent substitution of domestic capital goods in favor of imported capital goods. Also, the fact that India must operate and maintain an almost-permanent system of capital controls is something that would add greatly to its administrative costs. Moreover, the extent to which India’s bureaucracy has influence in the country and a lack of transparency both contribute to the difficulty the country faces in making solid policy decisions when operating capital controls. As a result, the governance costs associated with India’s capital controls are ones that should be considered when determining whether the benefits of these controls outweigh their costs (Patnaik and Shah, 2012). Another important factor that must be considered when assessing the effectiveness of India’s capital controls is the fact that the country has held a volatile capital control policy over the years. India has constantly altered its controls according the surrounding macroeconomic conditions—including 161 total capital control changes from 1998 to 2011—which has resulted in considerable instability for the country’s capital accounts (Hutchinson, Pasricha, and Singh, 2012, p. 396 and 404). Furthermore, even though India’s extensive use of capital controls was an attempt to adjust and maintain its balance of payments, the restrictions did not seem to help India as it experienced several balance of payments crises in recent decades (Callen and Cashin, 2002, p. 77) and experts fear it is on the verge of yet another crisis (Allen, 2013). Not only have India’s capital controls caused increased instability in the country’s capital markets, it has also contributed to the problem of extensive corruption in the country through a lack of bureaucratic transparency and large-scale government interventions in India’s capital markets (Kletzer, 2004, p. 264). Accordingly, India’s capital controls have proven to be both ineffective and costly, while India’s gradual relaxation of controls and move toward capital account liberalization has helped the economy grow significantly in the past few decades. It is crucial, therefore, that India pursues a capital account liberalization policy carefully and implements corresponding reforms where necessary to ensure as smooth a transition as possible.Continued on Next Page »

From the Inquiries Journal Blog  ") Related ReadingMonthly Newsletter SignupThe newsletter highlights recent selections from the journal and useful tips from our blog. Suggested Reading from Inquiries Journal

Inquiries Journal provides undergraduate and graduate students around the world a platform for the wide dissemination of academic work over a range of core disciplines. Representing the work of students from hundreds of institutions around the globe, Inquiries Journal's large database of academic articles is completely free. Learn more | Blog | Submit Follow IJ

Latest in Economics |