|

Featured Article: The Effect of Dodd-Frank on the Profitability of Community Banks: An Econometric Model

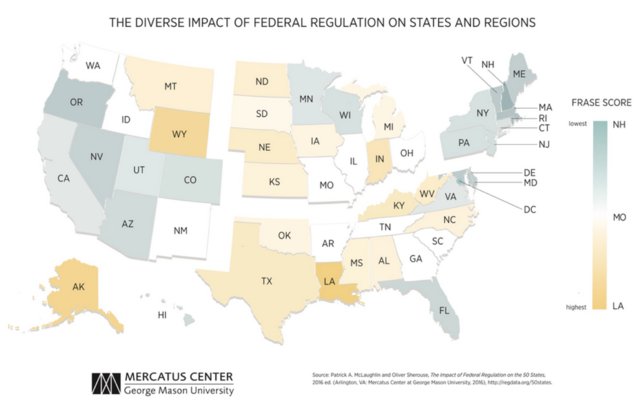

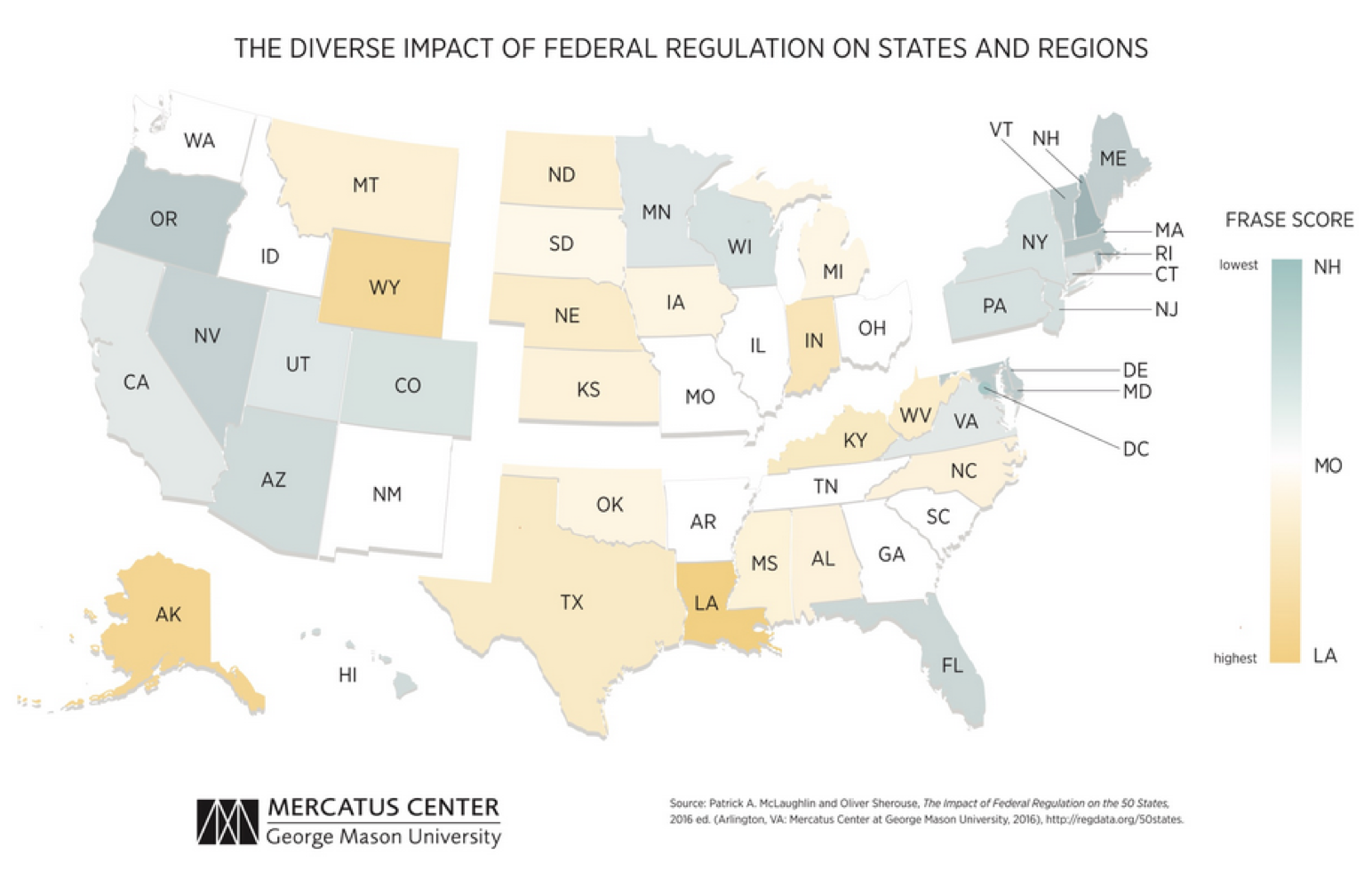

By examining explanatory variables for 82 banks in the years 2010-2014 factors affecting each dependent variable have been determined. Return on Equity is influenced negatively by growth of total deposits, cost efficiency, bank loan portfolio, non-performing loans, interest rate, and FRASE index, and positively affected by credit quality, assets, and real GDP. Return on Assets is influenced positively by the net interest margin, credit quality, and real GDP, and negatively by the FRASE index, non-performing loans, cost efficiency, and growth of total deposits. The Net Interest Margin is influenced negatively by inflation, and the interest rate and positively by non-performing loans. According to the models, there has been an impact on the profitability of banks since the enactment of the Dodd-Frank Act. This is evidenced by the negative correlation between profitability and the FRASE index. This correlation indicates that more regulation in a state decreases bank profitability. In addition, there was a positive correlation between asset size and profitability. This is interpreted as the smaller a bank is, the less profitable it will be. To conclude, a small bank and regulations will both negatively impact profitability. These findings are similar to findings by Naceur and Omran (2011). The Dodd-Frank Act requires more liquidity and there is evidence that holding deposits negatively affects profitability. However, the Dodd-Frank Act may have impacted the credit quality of banks and increased the quality of loans held. There is evidence that high quality loans increase profitability.

This study was based on the premise that the Dodd-Frank Act affects each of the explanatory variables and that these variables determine a bank’s return on equity, return on assets, and net interest margin. This study may be subject to omitted variable bias as there are many factors which may impact a bank’s profitability which were not included. It may be beneficial for future researchers to look into other regulations and their effects on different industries. In addition, sometime macroeconomic data is logged, however, it is not in this study. It may behoove a researcher to see if the data becomes more significant if it is logged. The economy was still recovering from a recession for the years available to sample; a more accurate study may be possible after the economy has recovered for a longer period. Eighty-two banks were used for this study, for future studies, larger and separate samples of community and non-community banks might lead to more accurate results.

Al-Ubaydli, O. & McLaughlin, P.A. (2015). RegData: A numerical database on industry-specific regulations for all United States industries and federal regulations, 1997-2012. Regulation & Governance, doi: 10.1111/rego.12107.

Arellano, M. & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies, 58.2, 277–297.

Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D. (2008). Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money, 18.2, 121-136.

Bloomberg L.P. (2015). Data. Retrieved from Bloomberg database.

Blundell, R. & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87, 115-143.

Board of Governors of the Federal Reserve System (US), 30-Year Conventional Mortgage Rate© [MORTG], retrieved from FRED, Federal Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/MORTG, April 25, 2016.

Dietrich, A., & Wanzenried, G., (2011). Determinants of bank profitability before and during the crisis: Evidence from Switzerland. Journal of Financial Markets, Institutions and Money, 21.3, 307-327.

Evans, L. (2012). Impact of the Dodd-Frank Act Depends Largely on Future Rule Making. United States Government Accountability Office, 12. N.p.

Federal Deposit Insurance Corporation. (2015). Deposit Market Share Reports. Retrieved from https://www5.fdic.gov/sod/sodMarketBank.asp?barItem=2

Kanas, A., Vasiliou, D., & Erotis, N. (2012). Revisiting bank profitability: A semi-parametric approach. Journal of International Financial Markets, Institutions and Money, 22.4, 990-1005.

Lux, M., & Greene, R. G. (2015). The State and Fate of Community Banking. Harvard Kennedy School. N.p.

Marsh, T. D., & Norman, J. W. (2012). The Impact of Dodd-Frank on Community Banks. Wake Forest University Legal Studies, Paper No. 2302392.

Naceur, S. B., & Omran, M. (2011). The Effects of Bank Regulations, Competition, And Financial Reforms on Banks' Performance. Emerging Markets Review, 12.1, 1-20.

Ozkan, S., Balsari, C. K., & Varan, S. (2014). Effect of Banking Regulation On Performance: Evidence from Turkey. Emerging Markets Finance & Trade, 50.4, 196-211.

Pierce, H., Robinson, I., & Stratmann, T. (2014). How Are Small Banks Faring Under Dodd-Frank?" George Mason University, N.p.

Pierce, H., & Miller, S. M. (2015). Small Banks by the Numbers. Mercatus Center, 2000–2014. N.p.

US. Bureau of Labor Statistics. Consumer Price Index for All Urban Consumers: All Items [CPIAUCSL], retrieved from FRED, Federal Reserve Bank of St. Louis. https://research.stlouisfed.org/fred2/series/CPIAUCSL, April 25, 2016.

US. Bureau of Economic Analysis. Real Gross Domestic Product [A191RL1Q225SBEA], retrieved from FRED, Federal Reserve Bank of St. Louis. https://research.stlouisfed.org/fred2/series/A191RL1Q225SBEA, April 25, 2016.

| Bank Code |

Bank Name |

State |

Community Bank |

| 1 |

Peoples United Bank |

CT |

No |

| 2 |

Webster Bank |

CT |

No |

| 3 |

PB Bancorp, Inc |

CT |

Yes |

| 4 |

Salisbury Bancorp, Inc. |

CT |

Yes |

| 5 |

SI Financial Group, Inc. |

CT |

Yes |

| 6 |

United Financial Bancorp, Inc. |

CT |

Yes |

| 7 |

Boston Private Financial Holdings, Inc. |

MA |

Yes |

| 8 |

Bershire Hills Bancorp, Inc. |

MA |

Yes |

| 9 |

Brookline Bancorp, Inc. |

MA |

Yes |

| 10 |

Chicopee Bancorp, Inc. |

MA |

Yes |

| 11 |

Century Bancorp, Inc. |

MA |

Yes |

| 12 |

Meridian Bancorp, Inc. |

MA |

Yes |

| 13 |

Enterprise Bank and Trust Company |

MA |

Yes |

| 14 |

Independent Bank Corp/MA |

MA |

Yes |

| 15 |

Westfield Finanacial, Inc |

MA |

Yes |

| 16 |

Bar Harbor Bank & Trust |

ME |

Yes |

| 17 |

Camden National Corporation |

ME |

Yes |

| 18 |

First Bancorp, Inc. |

ME |

Yes |

| 19 |

Northeast Bancorp |

ME |

Yes |

| 20 |

Lake Sunapee Bank Group |

NH |

Yes |

| 21 |

Hudson City Bancorp |

NJ |

No |

| 22 |

Valley National Bancorp |

NJ |

No |

| 23 |

BCB Bancorp Inc |

NJ |

Yes |

| 24 |

First Constitution Bancorp |

NJ |

Yes |

| 25 |

Cape Bancorp, Inc. |

NJ |

Yes |

| 26 |

ConnectOne Bancorp |

NJ |

Yes |

| 27 |

Lakeland Bancorp |

NJ |

Yes |

| 28 |

Maguyar Bancorp, Inc |

NJ |

Yes |

| 29 |

Northfield Bancorp, Inc. |

NJ |

Yes |

| 30 |

OceanFirst Financial Corp. |

NJ |

Yes |

| 31 |

Oritani Financial Corp |

NJ |

Yes |

| 32 |

Ocean Shore Holding Co. |

NJ |

Yes |

| 33 |

Providnet Financial Services, Inc |

NJ |

Yes |

| 34 |

Peapack-Gladstone Financial |

NJ |

Yes |

| 35 |

Parke Bancorp |

NJ |

Yes |

| 36 |

Sussex Bancorp |

NJ |

Yes |

| 37 |

Stewardship Financial Corporation |

NJ |

Yes |

| 38 |

Two River Bancorp |

NJ |

Yes |

| 39 |

Unity Bancorp, Inc |

NJ |

Yes |

| 40 |

Bank of NY Mellon |

NY |

No |

| 41 |

Citigroup |

NY |

No |

| 42 |

First Niagara Financial Group Inc. |

NY |

No |

| 43 |

M&T Bank Corp |

NY |

No |

| 44 |

New York Community Bancorp, Inc |

NY |

No |

| 45 |

JPMorgan Chase & Co |

NY |

No |

| 46 |

Signature Bank |

NY |

No |

| 47 |

The Bridgehampton National Bank |

NY |

Yes |

| 48 |

Financial Institutions |

NY |

Yes |

| 49 |

TrustCo Bank Corp |

NY |

Yes |

| 50 |

Arrow Financial Corp |

NY |

Yes |

| 51 |

Chemung Financial Corp |

NY |

Yes |

| 52 |

First of Long Island Corp |

NY |

Yes |

| 53 |

Flusing Financial Corp |

NY |

Yes |

| 54 |

Suffolk Bancorp |

NY |

Yes |

| 55 |

Tompkins Financial Corp |

NY |

Yes |

| 56 |

FNB Corp |

PA |

No |

| 57 |

Fulton Financial Corp |

PA |

No |

| 58 |

PNC Financial Services Group |

PA |

No |

| 59 |

Bryn Mawr Bank Corp |

PA |

Yes |

| 60 |

First Commonwealth Financial Corp |

PA |

Yes |

| 61 |

Orrstown Financial Services, Inc |

PA |

Yes |

| 62 |

S&T Bancorp Inc |

PA |

Yes |

| 63 |

Univest Corp of Pennsylvania |

PA |

Yes |

| 64 |

ACNB Bank |

PA |

Yes |

| 65 |

AmeriServ Financial Inc. |

PA |

Yes |

| 66 |

Beneficial Bancorp Inc |

PA |

Yes |

| 67 |

CNB Financial Corp |

PA |

Yes |

| 68 |

Codorus Valley Bancorp |

PA |

Yes |

| 69 |

First Citizens Community Bank |

PA |

Yes |

| 70 |

DNB First, National Association |

PA |

Yes |

| 71 |

The Fidelity Deposit and Discount Bank |

PA |

Yes |

| 72 |

First Keystone Community Bank |

PA |

Yes |

| 73 |

Republic First Bancorp, Inc |

PA |

Yes |

| 74 |

Fox Chase Bancorp, Inc. |

PA |

Yes |

| 75 |

Mid Penn Bank |

PA |

Yes |

| 76 |

National Penn Bancshares |

PA |

Yes |

| 77 |

Northwest Bancshares |

PA |

Yes |

| 78 |

Norwood Fianncial Corp |

PA |

Yes |

| 79 |

Prudential Bancorp |

PA |

Yes |

| 80 |

Penns Wood Bancorp |

PA |

Yes |

| 81 |

QNB Bank |

PA |

Yes |

| 82 |

Royal Bancshares of Pennsylvania, Inc |

PA |

Yes |

| Variable |

Measure |

Notation |

Expected Effect |

| Return on Equity |

Net income / average common equity |

ROE |

|

| Return on Assets |

Net income / average assets |

ROA |

|

| Net Interest Margin |

Net interest income / earnings assets |

NIM |

|

| Bank Code |

Corresponding code with each bank's name |

BCode |

? |

| Time Code |

Corresponding code with each time period |

TCode |

? |

| Community Bank Status |

<10 billion in assets is considered a community bank |

BankStatus |

- |

| Total Deposit Growth |

The percentage change over a one year period of total deposits |

TotDepG |

? |

| Interest Income Share |

The percentage of interest based income divided by non-interest income |

IntIncShare |

? |

| Cost Efficiency |

Total operating expenses / total revenue + total deposits |

CostEff |

- |

| Credit Quality |

Reserve for loan loss / total loans |

CreditQual |

+ |

| Diversification |

(Non-interest income / gross income)^2 / (interest income / gross income)^2 |

Div |

? |

| Bank Portfolio |

Total consumer loans / total commercial loans |

BankPort |

? |

| Non-performing loans |

Sequential growth from year before of loans in default (that do not accrue interest) |

NonPerG |

- |

| Herfindahl-Hirschman Index |

The market shares of each state that the bank are headquartered |

HHI |

? |

| Consumer Price Index |

The percentage change of the CPI lagged one period for all urban consumers in the Northeast |

CPI |

+ |

| Interest Rate |

The percentage change of the 30 year annual interest rate lagged one year |

IntRate |

+ |

| Real Gross Domestic Product |

The percentage change of RGDP each year |

RGDP |

+ |

| Assets |

The bank’s total assets for each year |

ASSETS |

? |

| Log Assets |

The bank’s total assets for each year logged |

LOGASSETS |

? |

| FRASE Current Index |

Ratio of the impact of federal regulations on a specific state’s industry to impact of regulation on the nation |

FRASECUR |

- |

| |

Mean |

Median |

Maximum |

Minimum |

Std. Dev. |

|

| ROA |

0.71 |

0.79 |

2.46 |

-2.87 |

0.54 |

|

| ROE |

6.73 |

7.78 |

26.65 |

-52.44 |

6.81 |

|

| NIM |

3.46 |

3.47 |

6.66 |

1.19 |

0.59 |

|

| CREDITQUAL |

1.45 |

1.32 |

5.98 |

0.00 |

0.66 |

|

| DIV |

2,692,880 |

0.45 |

157,000,000 |

0.00 |

17,352,034 |

|

| BANKPORT |

8.44 |

0.58 |

930.96 |

0.01 |

72.48 |

|

| INTINCSHARE |

6.73 |

4.78 |

163.95 |

-85.37 |

14.32 |

|

| TOTDEPG |

7.59 |

4.97 |

132.46 |

-23.53 |

13.89 |

|

| COSTEFF |

0.01 |

0.01 |

0.03 |

0.00 |

0.00 |

|

| NPLG |

5.78 |

-3.25 |

1871.20 |

-68.95 |

101.93 |

|

| HHI |

970.58 |

769.77 |

1740.00 |

476.11 |

343.48 |

|

| RGDP |

0.02 |

0.02 |

0.03 |

0.01 |

0.01 |

|

| CPI |

0.33 |

0.02 |

1.59 |

-0.13 |

0.63 |

|

| INTRATE |

-0.03 |

-0.13 |

0.33 |

-0.16 |

0.19 |

|

| ASSETS |

64979.82 |

1805.369 |

2572274 |

445.578 |

330234 |

| LOGASSETS |

3.481498 |

3.256504 |

6.410317 |

2.648924 |

0.758645 |

| FRASECUR |

1.18414 |

1.196959 |

1.291662 |

0.892552 |

0.07188 |

| Dependent Variable: |

Return on Equity |

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

| |

Regressor |

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Lagged ROE |

-0.222379 |

*** |

|

|

|

|

|

|

|

|

| T-Statistics |

|

-4.641318 |

|

|

|

|

|

|

|

|

|

| P-Values |

|

0.0000 |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Growth of Total Deposits |

0.042634 |

*** |

0.017546 |

|

-0.088893 |

*** |

|

|

-0.024719 |

*** |

| T-Statistics |

|

3.120637 |

|

-1.530967 |

|

-2.684342 |

|

|

|

-2.789861 |

|

| P-Values |

|

0.0019 |

|

0.1271 |

|

0.0078 |

|

|

|

0.0057 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Income Share |

0.002709 |

|

0.014365 |

|

|

|

|

|

0.053697 |

* |

| T-Statistics |

|

0.2229633 |

|

1.150026 |

|

|

|

|

|

1.853102 |

|

| P-Values |

|

0.8186 |

|

0.2513 |

|

|

|

|

|

0.0651 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Cost Efficiency |

-204.8525 |

|

-765.8297 |

*** |

|

|

|

|

-722.0357 |

*** |

| T-Statistics |

|

-1.184075 |

|

-7.28034 |

|

|

|

|

|

-4.593356 |

|

| P-Values |

|

0.2376 |

|

0 |

|

|

|

|

|

0.0000 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Credit Quality |

0.744468 |

|

4.740938 |

*** |

1.773751 |

|

2.127958 |

* |

|

|

| T-Statistics |

|

0.953958 |

|

2.654656 |

|

1.473657 |

|

1.914029 |

|

|

|

| P-Values |

|

0.3411 |

|

0.0085 |

|

0.1419 |

|

0.0568 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Diversification |

4.51E-09 |

|

3.23E-09 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.209837 |

|

0.501367 |

|

|

|

|

|

|

|

| P-Values |

|

0.834 |

|

0.6166 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Bank Loan Portfolio |

0.004794 |

** |

0.000723 |

|

-0.007029 |

*** |

-0.005287 |

*** |

|

|

| T-Statistics |

|

2.214442 |

|

0.159839 |

|

-5.887582 |

|

-11.84652 |

|

|

|

| P-Values |

|

0.0278 |

|

0.8731 |

|

0.0000 |

|

0.0000 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Non-Performing Loans |

0.001342 |

*** |

-0.001771 |

* |

-0.002343 |

** |

|

|

|

|

| T-Statistics |

|

5.487847 |

|

-1.861327 |

|

-2.081315 |

|

|

|

|

|

| P-Values |

|

0.0000 |

|

0.064 |

|

0.0385 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Market Concentration |

-0.003152 |

** |

0.000648 |

|

-0.002475 |

|

0.000163 |

|

|

|

| T-Statistics |

|

-2.410379 |

|

0.297074 |

|

-0.792956 |

|

0.089649 |

|

|

|

| P-Values |

|

0.0167 |

|

0.7667 |

|

0.4286 |

|

0.9286 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Inflation |

-218.384 |

*** |

-0.114589 |

|

|

|

|

|

|

|

| T-Statistics |

|

-16.29475 |

|

-0.25318 |

|

|

|

|

|

|

|

| P-Values |

|

0.0000 |

|

0.8004 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Rate |

1.152717 |

** |

-2.984662 |

** |

|

|

0.914768 |

** |

|

|

| T-Statistics |

|

2.037336 |

|

-2.318289 |

|

|

|

1.966565 |

|

|

|

| P-Values |

|

0.0428 |

|

0.0213 |

|

|

|

0.0504 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Change in RGDP |

2.917723 |

*** |

194.0825 |

*** |

|

|

|

|

|

|

| T-Statistics |

|

0.085212 |

|

2.560604 |

|

|

|

|

|

|

|

| P-Values |

|

0.9322 |

|

0.0111 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

FRASE Current |

26.20471 |

* |

-84.99074 |

*** |

-15.12968 |

|

|

|

|

|

| T-Statistics |

|

1.694851 |

|

-2.399252 |

|

-0.870833 |

|

|

|

|

|

| P-Values |

|

0.0914 |

|

0.0172 |

|

0.3847 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Assets |

|

|

0.0000425 |

|

0.001809 |

*** |

|

|

|

|

| T-Statistics |

|

|

|

0.826166 |

|

2.901016 |

|

|

|

|

|

| P-Values |

|

|

|

0.4096 |

|

0.0041 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Log Assets |

-42.43464 |

*** |

|

|

|

|

|

|

|

|

| T-Statistics |

|

-6.355648 |

|

|

|

|

|

|

|

|

|

| P-Values |

|

0.0000 |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

Wald-test (x2) |

154.92 |

|

13.57753 |

|

74.94697 |

|

70.59398 |

|

17.1347 |

|

| |

P-value |

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

| |

Degrees of Freedom |

(14,232) |

|

(13,233) |

|

(7,239) |

|

(4,242) |

|

(3,243) |

|

| |

AB test AR(1) (p-value) |

0.2542 |

|

0.1213 |

|

0.0002 |

*** |

0.1128 |

|

0.1131 |

|

| |

AB test AR(2) (p-value) |

0.9036 |

|

0.2354 |

|

0.376 |

|

0.2852 |

|

0.2576 |

|

| |

J-statistic |

28.63165 |

|

13.27295 |

|

19.95601 |

|

16.9328 |

|

13.44474 |

|

| Dependent Variable: |

Return on Assets |

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

| |

Regressor |

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Lagged ROA |

-0.11401 |

*** |

|

|

|

|

-0.163621 |

|

|

|

| T-Statistics |

|

-3.330133 |

|

|

|

|

|

-5.606098 |

|

|

|

| P-Values |

|

0.001 |

|

|

|

|

|

0.0000 |

*** |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Growth of Total Deposits |

-0.003856 |

*** |

-0.001541 |

|

-0.001688 |

** |

|

|

|

|

| T-Statistics |

|

-6.394816 |

|

-1.519691 |

|

-1.96318 |

|

|

|

|

|

| P-Values |

|

0.000 |

|

0.1300 |

|

0.0508 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Income Share |

-0.001538 |

|

0.00179 |

|

0.001819 |

*** |

|

|

|

|

| T-Statistics |

|

-1.386022 |

|

1.27512 |

|

4.525778 |

|

|

|

|

|

| P-Values |

|

0.1671 |

|

0.2035 |

|

0.0000 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Cost Efficiency |

-46.10715 |

*** |

-70.00679 |

*** |

-69.3976 |

*** |

|

|

|

|

| T-Statistics |

|

-4.319749 |

|

-11.49931 |

|

-10.40749 |

|

|

|

|

|

| P-Values |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Credit Quality |

0.132974 |

* |

0.525914 |

*** |

0.55464 |

*** |

0.208041 |

*** |

0.227217 |

** |

| T-Statistics |

|

1.659269 |

|

2.735755 |

|

3.073517 |

|

4.391417 |

|

2.441165 |

|

| P-Values |

|

0.0984 |

|

0.0067 |

|

0.0024 |

|

0.0000 |

|

0.0154 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Diversification |

5.73E-10 |

|

1.45E-10 |

|

|

|

6.94E-10 |

|

-1.53E-09 |

|

| T-Statistics |

|

0.409704 |

|

0.179957 |

|

|

|

0.628326 |

|

-1.570014 |

|

| P-Values |

|

0.6824 |

|

0.8573 |

|

|

|

0.5304 |

|

0.1177 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Bank Loan Portfolio |

-0.000107 |

|

1.65E-05 |

|

|

|

0.000178 |

|

-0.000554 |

*** |

| T-Statistics |

|

-0.805297 |

|

0.063815 |

|

|

|

1.047966 |

|

-8.20177 |

|

| P-Values |

|

0.4215 |

|

0.9492 |

|

|

|

0.2957 |

|

0.0000 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Non-Performing Loans |

-6.52E-05 |

|

-0.000112 |

** |

-0.000136 |

** |

|

|

|

|

| T-Statistics |

|

-1.151886 |

|

-2.111089 |

|

-2.340998 |

|

|

|

|

|

| P-Values |

|

0.2506 |

|

0.0358 |

|

0.0201 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Market Concentration |

-0.00029 |

|

-0.00011 |

|

|

|

|

|

|

|

| T-Statistics |

|

-1.594879 |

|

-0.473904 |

|

|

|

|

|

|

|

| P-Values |

|

0.1121 |

|

0.636 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Inflation |

-8.384053 |

|

0.001042 |

|

|

|

|

|

0.034889 |

|

| T-Statistics |

|

-8.407179 |

|

0.025535 |

|

|

|

|

|

1.13654 |

|

| P-Values |

|

0.0000 |

|

0.9797 |

|

|

|

|

|

0.2569 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Rate |

0.094854 |

|

-0.186681 |

|

-0.221118 |

** |

0.083999 |

** |

0.050837 |

|

| T-Statistics |

|

1.665884 |

|

-1.252933 |

|

-1.968304 |

|

2.207945 |

|

1.14635 |

|

| P-Values |

|

0.0971 |

|

0.2115 |

|

0.0502 |

|

0.0282 |

|

0.2528 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Change in RGDP |

-0.661256 |

|

14.82982 |

* |

15.78036 |

** |

|

|

|

|

| T-Statistics |

|

-0.265494 |

|

1.740556 |

|

2.484227 |

|

|

|

|

|

| P-Values |

|

0.7909 |

|

0.0831 |

|

0.0137 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

FRASE Current |

-0.951036 |

|

-7.303051 |

* |

-8.005292 |

** |

|

|

|

|

| T-Statistics |

|

-0.746545 |

|

-1.924799 |

|

-2.723464 |

|

|

|

|

|

| P-Values |

|

0.4561 |

|

0.0555 |

|

0.0069 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Assets |

1.93E-07 |

|

3.69E-06 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.255622 |

|

1.016637 |

|

|

|

|

|

|

|

| P-Values |

|

0.7985 |

|

0.3104 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

NIM |

0.425958 |

|

0.237762 |

** |

0.221161 |

*** |

|

|

|

|

| T-Statistics |

|

2.81375 |

|

2.217571 |

|

2.512385 |

|

|

|

|

|

| P-Values |

|

0.0053 |

|

0.0276 |

|

0.0127 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

Wald-test (x2) |

22.04917 |

|

24.87189 |

|

42.53674 |

|

17.33273 |

|

16.62161 |

|

| |

P-value |

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

| |

Degrees of Freedom |

(15,231) |

|

(14,232) |

|

(9,237) |

|

(6,240) |

|

(5,241) |

|

| |

AB test AR(1) (p-value) |

0.1021 |

|

0.711 |

|

0.0748 |

* |

0.6988 |

|

0.0686 |

* |

| |

AB test AR(2) (p-value) |

0.8278 |

|

0.3571 |

|

0.3628 |

|

0.5684 |

|

0.657 |

|

| Dependent Variable: |

Net Interest Margin |

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

| |

Regressor |

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Lagged NIM |

-0.135579 |

*** |

|

|

|

|

|

|

|

|

| T-Statistics |

|

-4.419571 |

|

|

|

|

|

|

|

|

|

| P-Values |

|

0 |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Growth of Total Deposits |

0.001211 |

|

0.0072 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.83382 |

|

0.477729 |

|

|

|

|

|

|

|

| P-Values |

|

0.4052 |

|

0.6333 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Income Share |

0.001625 |

|

-0.000485 |

|

-0.000971 |

|

|

|

-0.000753 |

|

| T-Statistics |

|

1.559869 |

|

-0.359968 |

|

-1.450526 |

|

|

|

-0.513956 |

|

| P-Values |

|

0.1202 |

|

0.7192 |

|

0.1482 |

|

|

|

0.6078 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Cost Efficiency |

-5.404967 |

|

1.361259 |

|

|

|

-4.227795 |

|

1.297272 |

|

| T-Statistics |

|

-1.436229 |

|

0.208903 |

|

|

|

-0.555831 |

|

0.257015 |

|

| P-Values |

|

0.1523 |

|

0.8347 |

|

|

|

0.5788 |

|

0.7974 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Credit Quality |

0.065634 |

|

0.058518 |

|

|

|

0.102466 |

|

|

|

| T-Statistics |

|

1.0544747 |

|

0.528938 |

|

|

|

0.811536 |

|

|

|

| P-Values |

|

0.2926 |

|

0.5974 |

|

|

|

0.4179 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Diversification |

3.29E-10 |

|

-1.85E-10 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.0866369 |

|

-0.321003 |

|

|

|

|

|

|

|

| P-Values |

|

0.3872 |

|

0.7485 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Bank Loan Portfolio |

4.90E-04 |

*** |

-3.36E-05 |

|

|

|

|

|

|

|

| T-Statistics |

|

7.913676 |

|

-0.154244 |

|

|

|

|

|

|

|

| P-Values |

|

0 |

|

0.8776 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Non-Performing Loans |

0.000384 |

*** |

9.80E-05 |

|

0.000149 |

*** |

|

|

0.000162 |

*** |

| T-Statistics |

|

5.845872 |

|

2.611361 |

|

4.224368 |

|

|

|

3.520371 |

|

| P-Values |

|

0 |

|

0.0096 |

|

0.0000 |

|

|

|

0.0005 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Market Concentration |

0.000284 |

|

-0.000379 |

|

-0.000344 |

|

|

|

|

|

| T-Statistics |

|

1.083485 |

|

-1.231675 |

|

-1.49662 |

|

|

|

|

|

| P-Values |

|

0.2797 |

|

0.2193 |

|

0.1358 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Inflation |

7.285612 |

** |

-0.050034 |

|

-0.059862 |

** |

-0.05197 |

** |

|

|

| T-Statistics |

|

2.158094 |

|

-1.06382 |

|

-2.426619 |

|

-2.266222 |

|

|

|

| P-Values |

|

0.0319 |

|

0.2885 |

|

0.016 |

|

0.0243 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Rate |

-0.083257 |

|

-0.162524 |

|

-0.201545 |

*** |

|

|

|

|

| T-Statistics |

|

-0.831332 |

|

-1.009467 |

|

-4.936669 |

|

|

|

|

|

| P-Values |

|

0.4066 |

|

0.3138 |

|

0.0000 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Change in RGDP |

-6.836565 |

|

0.137335 |

|

|

|

|

|

|

|

| T-Statistics |

|

-1.357096 |

|

0.016532 |

|

|

|

|

|

|

|

| P-Values |

|

0.1761 |

|

0.9868 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

FRASE Current |

0.112943 |

|

1.068448 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.07641 |

|

0.304873 |

|

|

|

|

|

|

|

| P-Values |

|

0.9392 |

|

0.7607 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Assets |

0.00000158 |

*** |

7.83E-07 |

|

-5.80E-05 |

|

2.69E-05 |

|

|

|

| T-Statistics |

|

-4.69457 |

|

0.33901 |

|

-1.425494 |

|

0.58416 |

|

|

|

| P-Values |

|

0 |

|

0.7349 |

|

0.1553 |

|

0.5597 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Assets2 |

|

|

|

|

1.11E-11 |

|

-3.98E-12 |

|

|

|

| T-Statistics |

|

|

|

|

|

1.420814 |

|

-0.481378 |

|

|

|

| P-Values |

|

|

|

|

|

0.1567 |

|

0.6307 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Log Assets |

|

|

|

|

2.165943 |

** |

|

|

|

|

| T-Statistics |

|

|

|

|

|

2.466267 |

|

|

|

|

|

| P-Values |

|

|

|

|

|

0.0144 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

ROA |

|

|

0.138247 |

|

0.144513 |

*** |

|

|

-0.022064 |

|

| T-Statistics |

|

|

|

1.384181 |

|

3.782389 |

|

|

|

-0.267735 |

|

| P-Values |

|

|

|

0.1676 |

|

0.0002 |

|

|

|

0.7891 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

ROE |

|

|

-0.001807 |

|

|

|

0.003307 |

|

0.003685 |

|

| T-Statistics |

|

|

|

-0.394199 |

|

|

|

1.189613 |

|

0.853875 |

|

| P-Values |

|

|

|

0.6938 |

|

|

|

0.2354 |

|

0.394 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

Wald-test (x2) |

48.4524 |

|

102.2585 |

|

25.8496 |

|

3.078968 |

|

5.308015 |

|

| |

P-value |

0.0000 |

|

0.0000 |

|

0.000 |

|

0.0064 |

|

0.0001 |

|

| |

Degrees of Freedom |

(14,232) |

|

(15,231) |

|

(9,237) |

|

(6,240) |

|

(5,241) |

|

| |

AB test AR(1) (p-value) |

0.3215 |

|

0.1046 |

|

0.0896 |

|

0.1327 |

|

0.1202 |

|

| |

AB test AR(2) (p-value) |

0.616 |

|

0.104 |

|

0.0616 |

* |

0.1412 |

|

0.1504 |

|

| |

J-statistic |

20.2971 |

|

21.69154 |

|

14.98535 |

|

22.41962 |

|

32.3475 |

|

| |

Prob(J-statistic) |

0.009269 |

|

0.00991 |

|

0.452473 |

|

0.00764 |

|

0.000173 |

|

Al-Ubaydli, O. & McLaughlin, P.A. (2015). RegData: A numerical database on industry-specific regulations for all United States industries and federal regulations, 1997-2012. Regulation & Governance, doi: 10.1111/rego.12107.

Arellano, M. & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies, 58.2, 277–297.

Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D. (2008). Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money, 18.2, 121-136.

Bloomberg L.P. (2015). Data. Retrieved from Bloomberg database.

Blundell, R. & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87, 115-143.

Board of Governors of the Federal Reserve System (US), 30-Year Conventional Mortgage Rate© [MORTG], retrieved from FRED, Federal Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/MORTG, April 25, 2016.

Dietrich, A., & Wanzenried, G., (2011). Determinants of bank profitability before and during the crisis: Evidence from Switzerland. Journal of Financial Markets, Institutions and Money, 21.3, 307-327.

Evans, L. (2012). Impact of the Dodd-Frank Act Depends Largely on Future Rule Making. United States Government Accountability Office, 12. N.p.

Federal Deposit Insurance Corporation. (2015). Deposit Market Share Reports. Retrieved from https://www5.fdic.gov/sod/sodMarketBank.asp?barItem=2

Kanas, A., Vasiliou, D., & Erotis, N. (2012). Revisiting bank profitability: A semi-parametric approach. Journal of International Financial Markets, Institutions and Money, 22.4, 990-1005.

Lux, M., & Greene, R. G. (2015). The State and Fate of Community Banking. Harvard Kennedy School. N.p.

Marsh, T. D., & Norman, J. W. (2012). The Impact of Dodd-Frank on Community Banks. Wake Forest University Legal Studies, Paper No. 2302392.

Naceur, S. B., & Omran, M. (2011). The Effects of Bank Regulations, Competition, And Financial Reforms on Banks' Performance. Emerging Markets Review, 12.1, 1-20.

Ozkan, S., Balsari, C. K., & Varan, S. (2014). Effect of Banking Regulation On Performance: Evidence from Turkey. Emerging Markets Finance & Trade, 50.4, 196-211.

Pierce, H., Robinson, I., & Stratmann, T. (2014). How Are Small Banks Faring Under Dodd-Frank?" George Mason University, N.p.

Pierce, H., & Miller, S. M. (2015). Small Banks by the Numbers. Mercatus Center, 2000–2014. N.p.

US. Bureau of Labor Statistics. Consumer Price Index for All Urban Consumers: All Items [CPIAUCSL], retrieved from FRED, Federal Reserve Bank of St. Louis. https://research.stlouisfed.org/fred2/series/CPIAUCSL, April 25, 2016.

US. Bureau of Economic Analysis. Real Gross Domestic Product [A191RL1Q225SBEA], retrieved from FRED, Federal Reserve Bank of St. Louis. https://research.stlouisfed.org/fred2/series/A191RL1Q225SBEA, April 25, 2016.

Appendix A: Banks & Locations Data

| Bank Code |

Bank Name |

State |

Community Bank |

| 1 |

Peoples United Bank |

CT |

No |

| 2 |

Webster Bank |

CT |

No |

| 3 |

PB Bancorp, Inc |

CT |

Yes |

| 4 |

Salisbury Bancorp, Inc. |

CT |

Yes |

| 5 |

SI Financial Group, Inc. |

CT |

Yes |

| 6 |

United Financial Bancorp, Inc. |

CT |

Yes |

| 7 |

Boston Private Financial Holdings, Inc. |

MA |

Yes |

| 8 |

Bershire Hills Bancorp, Inc. |

MA |

Yes |

| 9 |

Brookline Bancorp, Inc. |

MA |

Yes |

| 10 |

Chicopee Bancorp, Inc. |

MA |

Yes |

| 11 |

Century Bancorp, Inc. |

MA |

Yes |

| 12 |

Meridian Bancorp, Inc. |

MA |

Yes |

| 13 |

Enterprise Bank and Trust Company |

MA |

Yes |

| 14 |

Independent Bank Corp/MA |

MA |

Yes |

| 15 |

Westfield Finanacial, Inc |

MA |

Yes |

| 16 |

Bar Harbor Bank & Trust |

ME |

Yes |

| 17 |

Camden National Corporation |

ME |

Yes |

| 18 |

First Bancorp, Inc. |

ME |

Yes |

| 19 |

Northeast Bancorp |

ME |

Yes |

| 20 |

Lake Sunapee Bank Group |

NH |

Yes |

| 21 |

Hudson City Bancorp |

NJ |

No |

| 22 |

Valley National Bancorp |

NJ |

No |

| 23 |

BCB Bancorp Inc |

NJ |

Yes |

| 24 |

First Constitution Bancorp |

NJ |

Yes |

| 25 |

Cape Bancorp, Inc. |

NJ |

Yes |

| 26 |

ConnectOne Bancorp |

NJ |

Yes |

| 27 |

Lakeland Bancorp |

NJ |

Yes |

| 28 |

Maguyar Bancorp, Inc |

NJ |

Yes |

| 29 |

Northfield Bancorp, Inc. |

NJ |

Yes |

| 30 |

OceanFirst Financial Corp. |

NJ |

Yes |

| 31 |

Oritani Financial Corp |

NJ |

Yes |

| 32 |

Ocean Shore Holding Co. |

NJ |

Yes |

| 33 |

Providnet Financial Services, Inc |

NJ |

Yes |

| 34 |

Peapack-Gladstone Financial |

NJ |

Yes |

| 35 |

Parke Bancorp |

NJ |

Yes |

| 36 |

Sussex Bancorp |

NJ |

Yes |

| 37 |

Stewardship Financial Corporation |

NJ |

Yes |

| 38 |

Two River Bancorp |

NJ |

Yes |

| 39 |

Unity Bancorp, Inc |

NJ |

Yes |

| 40 |

Bank of NY Mellon |

NY |

No |

| 41 |

Citigroup |

NY |

No |

| 42 |

First Niagara Financial Group Inc. |

NY |

No |

| 43 |

M&T Bank Corp |

NY |

No |

| 44 |

New York Community Bancorp, Inc |

NY |

No |

| 45 |

JPMorgan Chase & Co |

NY |

No |

| 46 |

Signature Bank |

NY |

No |

| 47 |

The Bridgehampton National Bank |

NY |

Yes |

| 48 |

Financial Institutions |

NY |

Yes |

| 49 |

TrustCo Bank Corp |

NY |

Yes |

| 50 |

Arrow Financial Corp |

NY |

Yes |

| 51 |

Chemung Financial Corp |

NY |

Yes |

| 52 |

First of Long Island Corp |

NY |

Yes |

| 53 |

Flusing Financial Corp |

NY |

Yes |

| 54 |

Suffolk Bancorp |

NY |

Yes |

| 55 |

Tompkins Financial Corp |

NY |

Yes |

| 56 |

FNB Corp |

PA |

No |

| 57 |

Fulton Financial Corp |

PA |

No |

| 58 |

PNC Financial Services Group |

PA |

No |

| 59 |

Bryn Mawr Bank Corp |

PA |

Yes |

| 60 |

First Commonwealth Financial Corp |

PA |

Yes |

| 61 |

Orrstown Financial Services, Inc |

PA |

Yes |

| 62 |

S&T Bancorp Inc |

PA |

Yes |

| 63 |

Univest Corp of Pennsylvania |

PA |

Yes |

| 64 |

ACNB Bank |

PA |

Yes |

| 65 |

AmeriServ Financial Inc. |

PA |

Yes |

| 66 |

Beneficial Bancorp Inc |

PA |

Yes |

| 67 |

CNB Financial Corp |

PA |

Yes |

| 68 |

Codorus Valley Bancorp |

PA |

Yes |

| 69 |

First Citizens Community Bank |

PA |

Yes |

| 70 |

DNB First, National Association |

PA |

Yes |

| 71 |

The Fidelity Deposit and Discount Bank |

PA |

Yes |

| 72 |

First Keystone Community Bank |

PA |

Yes |

| 73 |

Republic First Bancorp, Inc |

PA |

Yes |

| 74 |

Fox Chase Bancorp, Inc. |

PA |

Yes |

| 75 |

Mid Penn Bank |

PA |

Yes |

| 76 |

National Penn Bancshares |

PA |

Yes |

| 77 |

Northwest Bancshares |

PA |

Yes |

| 78 |

Norwood Fianncial Corp |

PA |

Yes |

| 79 |

Prudential Bancorp |

PA |

Yes |

| 80 |

Penns Wood Bancorp |

PA |

Yes |

| 81 |

QNB Bank |

PA |

Yes |

| 82 |

Royal Bancshares of Pennsylvania, Inc |

PA |

Yes |

Appendix B: Correlation Matrix Appendix C Variable Descriptions

| Variable |

Measure |

Notation |

Expected Effect |

| Return on Equity |

Net income / average common equity |

ROE |

|

| Return on Assets |

Net income / average assets |

ROA |

|

| Net Interest Margin |

Net interest income / earnings assets |

NIM |

|

| Bank Code |

Corresponding code with each bank's name |

BCode |

? |

| Time Code |

Corresponding code with each time period |

TCode |

? |

| Community Bank Status |

<10 billion in assets is considered a community bank |

BankStatus |

- |

| Total Deposit Growth |

The percentage change over a one year period of total deposits |

TotDepG |

? |

| Interest Income Share |

The percentage of interest based income divided by non-interest income |

IntIncShare |

? |

| Cost Efficiency |

Total operating expenses / total revenue + total deposits |

CostEff |

- |

| Credit Quality |

Reserve for loan loss / total loans |

CreditQual |

+ |

| Diversification |

(Non-interest income / gross income)^2 / (interest income / gross income)^2 |

Div |

? |

| Bank Portfolio |

Total consumer loans / total commercial loans |

BankPort |

? |

| Non-performing loans |

Sequential growth from year before of loans in default (that do not accrue interest) |

NonPerG |

- |

| Herfindahl-Hirschman Index |

The market shares of each state that the bank are headquartered |

HHI |

? |

| Consumer Price Index |

The percentage change of the CPI lagged one period for all urban consumers in the Northeast |

CPI |

+ |

| Interest Rate |

The percentage change of the 30 year annual interest rate lagged one year |

IntRate |

+ |

| Real Gross Domestic Product |

The percentage change of RGDP each year |

RGDP |

+ |

| Assets |

The bank’s total assets for each year |

ASSETS |

? |

| Log Assets |

The bank’s total assets for each year logged |

LOGASSETS |

? |

| FRASE Current Index |

Ratio of the impact of federal regulations on a specific state’s industry to impact of regulation on the nation |

FRASECUR |

- |

Appendix D: Descriptive Statistics

| |

Mean |

Median |

Maximum |

Minimum |

Std. Dev. |

|

| ROA |

0.71 |

0.79 |

2.46 |

-2.87 |

0.54 |

|

| ROE |

6.73 |

7.78 |

26.65 |

-52.44 |

6.81 |

|

| NIM |

3.46 |

3.47 |

6.66 |

1.19 |

0.59 |

|

| CREDITQUAL |

1.45 |

1.32 |

5.98 |

0.00 |

0.66 |

|

| DIV |

2,692,880 |

0.45 |

157,000,000 |

0.00 |

17,352,034 |

|

| BANKPORT |

8.44 |

0.58 |

930.96 |

0.01 |

72.48 |

|

| INTINCSHARE |

6.73 |

4.78 |

163.95 |

-85.37 |

14.32 |

|

| TOTDEPG |

7.59 |

4.97 |

132.46 |

-23.53 |

13.89 |

|

| COSTEFF |

0.01 |

0.01 |

0.03 |

0.00 |

0.00 |

|

| NPLG |

5.78 |

-3.25 |

1871.20 |

-68.95 |

101.93 |

|

| HHI |

970.58 |

769.77 |

1740.00 |

476.11 |

343.48 |

|

| RGDP |

0.02 |

0.02 |

0.03 |

0.01 |

0.01 |

|

| CPI |

0.33 |

0.02 |

1.59 |

-0.13 |

0.63 |

|

| INTRATE |

-0.03 |

-0.13 |

0.33 |

-0.16 |

0.19 |

|

| ASSETS |

64979.82 |

1805.369 |

2572274 |

445.578 |

330234 |

| LOGASSETS |

3.481498 |

3.256504 |

6.410317 |

2.648924 |

0.758645 |

| FRASECUR |

1.18414 |

1.196959 |

1.291662 |

0.892552 |

0.07188 |

Appendix E: ROE Dependent Variable: Model Results

| Dependent Variable: |

Return on Equity |

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

| |

Regressor |

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Lagged ROE |

-0.222379 |

*** |

|

|

|

|

|

|

|

|

| T-Statistics |

|

-4.641318 |

|

|

|

|

|

|

|

|

|

| P-Values |

|

0.0000 |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Growth of Total Deposits |

0.042634 |

*** |

0.017546 |

|

-0.088893 |

*** |

|

|

-0.024719 |

*** |

| T-Statistics |

|

3.120637 |

|

-1.530967 |

|

-2.684342 |

|

|

|

-2.789861 |

|

| P-Values |

|

0.0019 |

|

0.1271 |

|

0.0078 |

|

|

|

0.0057 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Income Share |

0.002709 |

|

0.014365 |

|

|

|

|

|

0.053697 |

* |

| T-Statistics |

|

0.2229633 |

|

1.150026 |

|

|

|

|

|

1.853102 |

|

| P-Values |

|

0.8186 |

|

0.2513 |

|

|

|

|

|

0.0651 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Cost Efficiency |

-204.8525 |

|

-765.8297 |

*** |

|

|

|

|

-722.0357 |

*** |

| T-Statistics |

|

-1.184075 |

|

-7.28034 |

|

|

|

|

|

-4.593356 |

|

| P-Values |

|

0.2376 |

|

0 |

|

|

|

|

|

0.0000 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Credit Quality |

0.744468 |

|

4.740938 |

*** |

1.773751 |

|

2.127958 |

* |

|

|

| T-Statistics |

|

0.953958 |

|

2.654656 |

|

1.473657 |

|

1.914029 |

|

|

|

| P-Values |

|

0.3411 |

|

0.0085 |

|

0.1419 |

|

0.0568 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Diversification |

4.51E-09 |

|

3.23E-09 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.209837 |

|

0.501367 |

|

|

|

|

|

|

|

| P-Values |

|

0.834 |

|

0.6166 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Bank Loan Portfolio |

0.004794 |

** |

0.000723 |

|

-0.007029 |

*** |

-0.005287 |

*** |

|

|

| T-Statistics |

|

2.214442 |

|

0.159839 |

|

-5.887582 |

|

-11.84652 |

|

|

|

| P-Values |

|

0.0278 |

|

0.8731 |

|

0.0000 |

|

0.0000 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Non-Performing Loans |

0.001342 |

*** |

-0.001771 |

* |

-0.002343 |

** |

|

|

|

|

| T-Statistics |

|

5.487847 |

|

-1.861327 |

|

-2.081315 |

|

|

|

|

|

| P-Values |

|

0.0000 |

|

0.064 |

|

0.0385 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Market Concentration |

-0.003152 |

** |

0.000648 |

|

-0.002475 |

|

0.000163 |

|

|

|

| T-Statistics |

|

-2.410379 |

|

0.297074 |

|

-0.792956 |

|

0.089649 |

|

|

|

| P-Values |

|

0.0167 |

|

0.7667 |

|

0.4286 |

|

0.9286 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Inflation |

-218.384 |

*** |

-0.114589 |

|

|

|

|

|

|

|

| T-Statistics |

|

-16.29475 |

|

-0.25318 |

|

|

|

|

|

|

|

| P-Values |

|

0.0000 |

|

0.8004 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Rate |

1.152717 |

** |

-2.984662 |

** |

|

|

0.914768 |

** |

|

|

| T-Statistics |

|

2.037336 |

|

-2.318289 |

|

|

|

1.966565 |

|

|

|

| P-Values |

|

0.0428 |

|

0.0213 |

|

|

|

0.0504 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Change in RGDP |

2.917723 |

*** |

194.0825 |

*** |

|

|

|

|

|

|

| T-Statistics |

|

0.085212 |

|

2.560604 |

|

|

|

|

|

|

|

| P-Values |

|

0.9322 |

|

0.0111 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

FRASE Current |

26.20471 |

* |

-84.99074 |

*** |

-15.12968 |

|

|

|

|

|

| T-Statistics |

|

1.694851 |

|

-2.399252 |

|

-0.870833 |

|

|

|

|

|

| P-Values |

|

0.0914 |

|

0.0172 |

|

0.3847 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Assets |

|

|

0.0000425 |

|

0.001809 |

*** |

|

|

|

|

| T-Statistics |

|

|

|

0.826166 |

|

2.901016 |

|

|

|

|

|

| P-Values |

|

|

|

0.4096 |

|

0.0041 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Log Assets |

-42.43464 |

*** |

|

|

|

|

|

|

|

|

| T-Statistics |

|

-6.355648 |

|

|

|

|

|

|

|

|

|

| P-Values |

|

0.0000 |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

Wald-test (x2) |

154.92 |

|

13.57753 |

|

74.94697 |

|

70.59398 |

|

17.1347 |

|

| |

P-value |

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

| |

Degrees of Freedom |

(14,232) |

|

(13,233) |

|

(7,239) |

|

(4,242) |

|

(3,243) |

|

| |

AB test AR(1) (p-value) |

0.2542 |

|

0.1213 |

|

0.0002 |

*** |

0.1128 |

|

0.1131 |

|

| |

AB test AR(2) (p-value) |

0.9036 |

|

0.2354 |

|

0.376 |

|

0.2852 |

|

0.2576 |

|

| |

J-statistic |

28.63165 |

|

13.27295 |

|

19.95601 |

|

16.9328 |

|

13.44474 |

|

Appendix F: ROA Dependent Variable: Model Results

| Dependent Variable: |

Return on Assets |

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

| |

Regressor |

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Lagged ROA |

-0.11401 |

*** |

|

|

|

|

-0.163621 |

|

|

|

| T-Statistics |

|

-3.330133 |

|

|

|

|

|

-5.606098 |

|

|

|

| P-Values |

|

0.001 |

|

|

|

|

|

0.0000 |

*** |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Growth of Total Deposits |

-0.003856 |

*** |

-0.001541 |

|

-0.001688 |

** |

|

|

|

|

| T-Statistics |

|

-6.394816 |

|

-1.519691 |

|

-1.96318 |

|

|

|

|

|

| P-Values |

|

0.000 |

|

0.1300 |

|

0.0508 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Income Share |

-0.001538 |

|

0.00179 |

|

0.001819 |

*** |

|

|

|

|

| T-Statistics |

|

-1.386022 |

|

1.27512 |

|

4.525778 |

|

|

|

|

|

| P-Values |

|

0.1671 |

|

0.2035 |

|

0.0000 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Cost Efficiency |

-46.10715 |

*** |

-70.00679 |

*** |

-69.3976 |

*** |

|

|

|

|

| T-Statistics |

|

-4.319749 |

|

-11.49931 |

|

-10.40749 |

|

|

|

|

|

| P-Values |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Credit Quality |

0.132974 |

* |

0.525914 |

*** |

0.55464 |

*** |

0.208041 |

*** |

0.227217 |

** |

| T-Statistics |

|

1.659269 |

|

2.735755 |

|

3.073517 |

|

4.391417 |

|

2.441165 |

|

| P-Values |

|

0.0984 |

|

0.0067 |

|

0.0024 |

|

0.0000 |

|

0.0154 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Diversification |

5.73E-10 |

|

1.45E-10 |

|

|

|

6.94E-10 |

|

-1.53E-09 |

|

| T-Statistics |

|

0.409704 |

|

0.179957 |

|

|

|

0.628326 |

|

-1.570014 |

|

| P-Values |

|

0.6824 |

|

0.8573 |

|

|

|

0.5304 |

|

0.1177 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Bank Loan Portfolio |

-0.000107 |

|

1.65E-05 |

|

|

|

0.000178 |

|

-0.000554 |

*** |

| T-Statistics |

|

-0.805297 |

|

0.063815 |

|

|

|

1.047966 |

|

-8.20177 |

|

| P-Values |

|

0.4215 |

|

0.9492 |

|

|

|

0.2957 |

|

0.0000 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Non-Performing Loans |

-6.52E-05 |

|

-0.000112 |

** |

-0.000136 |

** |

|

|

|

|

| T-Statistics |

|

-1.151886 |

|

-2.111089 |

|

-2.340998 |

|

|

|

|

|

| P-Values |

|

0.2506 |

|

0.0358 |

|

0.0201 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Market Concentration |

-0.00029 |

|

-0.00011 |

|

|

|

|

|

|

|

| T-Statistics |

|

-1.594879 |

|

-0.473904 |

|

|

|

|

|

|

|

| P-Values |

|

0.1121 |

|

0.636 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Inflation |

-8.384053 |

|

0.001042 |

|

|

|

|

|

0.034889 |

|

| T-Statistics |

|

-8.407179 |

|

0.025535 |

|

|

|

|

|

1.13654 |

|

| P-Values |

|

0.0000 |

|

0.9797 |

|

|

|

|

|

0.2569 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Interest Rate |

0.094854 |

|

-0.186681 |

|

-0.221118 |

** |

0.083999 |

** |

0.050837 |

|

| T-Statistics |

|

1.665884 |

|

-1.252933 |

|

-1.968304 |

|

2.207945 |

|

1.14635 |

|

| P-Values |

|

0.0971 |

|

0.2115 |

|

0.0502 |

|

0.0282 |

|

0.2528 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Change in RGDP |

-0.661256 |

|

14.82982 |

* |

15.78036 |

** |

|

|

|

|

| T-Statistics |

|

-0.265494 |

|

1.740556 |

|

2.484227 |

|

|

|

|

|

| P-Values |

|

0.7909 |

|

0.0831 |

|

0.0137 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

FRASE Current |

-0.951036 |

|

-7.303051 |

* |

-8.005292 |

** |

|

|

|

|

| T-Statistics |

|

-0.746545 |

|

-1.924799 |

|

-2.723464 |

|

|

|

|

|

| P-Values |

|

0.4561 |

|

0.0555 |

|

0.0069 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Assets |

1.93E-07 |

|

3.69E-06 |

|

|

|

|

|

|

|

| T-Statistics |

|

0.255622 |

|

1.016637 |

|

|

|

|

|

|

|

| P-Values |

|

0.7985 |

|

0.3104 |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| Coefficient |

NIM |

0.425958 |

|

0.237762 |

** |

0.221161 |

*** |

|

|

|

|

| T-Statistics |

|

2.81375 |

|

2.217571 |

|

2.512385 |

|

|

|

|

|

| P-Values |

|

0.0053 |

|

0.0276 |

|

0.0127 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

Wald-test (x2) |

22.04917 |

|

24.87189 |

|

42.53674 |

|

17.33273 |

|

16.62161 |

|

| |

P-value |

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

0.0000 |

|

| |

Degrees of Freedom |

(15,231) |

|

(14,232) |

|

(9,237) |

|

(6,240) |

|

(5,241) |

|

| |

AB test AR(1) (p-value) |

0.1021 |

|

0.711 |

|

0.0748 |

* |

0.6988 |

|

0.0686 |

* |

| |

AB test AR(2) (p-value) |

0.8278 |

|

0.3571 |

|

0.3628 |

|

0.5684 |

|

0.657 |

|

Appendix G: NIM Dependent Variable: Model Results

| Dependent Variable: |

Net Interest Margin |

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

| |

Regressor |

|

|

|

|

|

|

|

|

|

|

| Coefficient |

Lagged NIM |

-0.135579 |

*** |

|

|

|

|

|

|

|

|

| T-Statistics |

|

-4.419571 |

|

|

|

|

|

|

|

|

|

| P-Values |

|

0 |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|