Roosevelt's Recession: A Historical and Econometric Examination of the Roots of the 1937 Recession

The Disorientation of A Discipline

In response to the Depression, Keynes developed new economic theories that questioned an orthodoxy accepted for centuries in the English-speaking world. Until the early 1930s, classical economics was the prevailing school of thought in Britain, and to a lesser extent, the United States. The roots of classical economics can be traced to Adam Smith’s magnum opus, The Wealth of Nations (1776). Smith’s book made commonplace the belief that free markets were guided by an “invisible hand.”47 The history of economic thought is punctuated by pioneering figures, like Smith. These individuals fundamentally altered existing theories, and oftentimes, served as key public figureheads.

In the two decades leading up to 1930, Irving Fisher was as the center of American economics. Fisher studied at Yale and obtained his undergraduate degree in 1888 and his Ph.D. in 1891. At Yale, Fisher found himself surrounded by Progressive-Era economists who, unlike their British counterparts, largely rejected laissez-faire principles. Unlike economists today, mainstream economists in the late 1800’s had greater flexibility to hold reform-minded views because the profession had not yet fully professionalized, nor had it developed grounding in statistical analysis.

In 1896, Arthur Hadley, later to serve as President of Yale for twenty-two years, critically referred to American economists as “a large and influential body of men who are engaged in extending the functions of government.”48 49 Fisher strongly agreed with Hadley. During his studies, Fisher became increasingly disgruntled with the views of his peers and professors. Fisher’s theoretical interests stood in contrast of the reform-minded economists, like E.R.A. Seligman, who were at the forefront of American discourse during the three-decade period before the Great War.Fisher eventually found a comfortable niche at Yale. He tailored his studies and flocked to courses led by William Graham Sumner, the Chair of Political Economy. Sumner was a polarizing figure who held contrarian views; unlike his colleagues, Sumner was a staunch advocate of laissez-faire economics. Fisher leaned towards laissez-faire economic thought, and he believed the discipline should free itself from its early roots in philosophical inquiry. Fisher desired a rigorous analytic model of study that yielded conclusive answers; he wanted to push the field towards the realm of the sciences.50

Advertisement

Sumner advised Fisher to write a dissertation using mathematical economics, a field still in its infancy. Fisher believed that “before applying political economy to railway rates, to the problems of trusts, to the explanation of some current crisis, it is best to develop the theory of political economy in general.”51 Adhering to this desire, Fisher set out to create one of the first mathematical models of an economy. Fisher included a model in his dissertation, titled “Mathematical Investigations in the Theory of Value and Prices.” His thesis was widely and highly praised. Paul Samuelson, the first recipient of the Nobel Memorial Prize in Economics, proclaimed Fisher’s work as “the greatest doctoral dissertation in economics ever written.”52

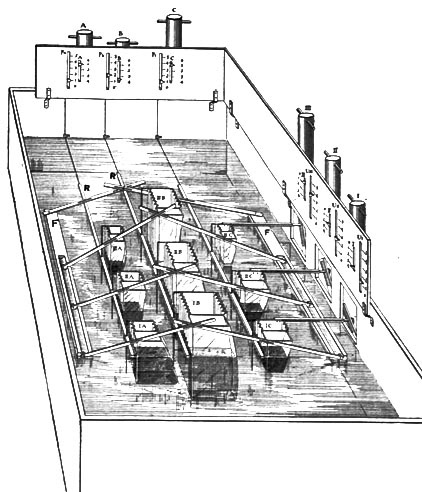

Fisher’s model was a hydraulic machine that calculated equilibrium prices. Fisher’s highly complicated hydraulic contraption was a simplified representation of the interrelated nature of the economy. Although a simplified rendition of the economy, the machine represented the markets at work. As Fisher grew older, he strayed from strict adherence to laissez-faire economics. In a 1906 piece, he declared that government had a role to play in the economy because markets could not always be trusted to act in the best interest of society. A middle ground was needed because, as he noted, "We are today in danger of too much socialistic experimentation; but nothing can be gained... by ignoring or condoning the opposite evils of individualism.”53 The idea he hints at is an externality, a concept formally introduced by Pigou in 1920.

{kind=link}

Figure 4. Diagram of Fisher's Equilibrium Machine. Source: Fisher, "Mathematical Investigations in the Theory," 38.

In the two decades since 1906, Fisher’s work in the field of monetary economics gained an audience in England with Keynes.54 Both Fisher and Keynes viewed the stability of a currency’s purchasing power as the antidote to gluts and instability.55

Fisher viewed not the gold standard problematic, but the way it was used; a unit of money was tied to a weight of gold, not to a unit of purchasing power. In regards to the price level, Fisher believed, "The so-called ‘level of prices’ is largely at the mercy of monetary and credit conditions. The tide of prices will rise or fall with the flood or ebb of gold or of paper money or of bank credit. Evidently a rise in the level of prices is a fall in the purchasing power of the dollar or other monetary unit, and vice versa.”56

To remedy this inherent instability, Fisher believed government had to maintain a constant purchasing power by varying the weight of a gold dollar. Under his proposal, the price of gold bullion would vary relative to commodity prices.

The recession experienced in 1920-1 inspired Fisher to relate fluctuations in the supply of money to booms and busts. World War One brought with it a 147% increase in the wholesale price level between June 1914 and May 1920.57 To combat inflation, the Federal Reserve Bank of New York rapidly increased the discount rate, and the system’s other banks followed New York’s lead. In the seven months between November 1919 and June 1920, the discount rate increased from 4% to 7%.58 The rate increase was unprecedented, and by 1921 it became evident that the Federal Reserve had achieved its goal of deflating the economy. Unfortunately, the economy deflated to an undesirable extent, and a deflationary recession was underway. Whether Lebergott’s or Romer’s historical unemployment rate calculations are considered, the unemployment rate essentially doubled between 1920 to 1921.59

The experience of 1921 led Fisher to explore the relation between the price level and unemployment. Whereas his predecessors found no link between the price level and the unemployment rate, Fisher uncovered the existence of a relationship between the rate of change of the price level and the unemployment rate.60 With this discovery, Fisher started to advocate for intervention aimed at price level stabilization. In a 1923 letter to the editor of the New York Times, Fisher criticized an editorial that argued against Keynes’ advocacy of price stabilization. In his letter, Fisher drew a distinction between prices and the price level. While “prices should be left to supply and demand,” Fisher noted that, “This does not, or should not, mean that the price level should be left to supply and demand.”61

Two years later, Fisher published an article where he argued that variations in economic activity, as measured by Warren M. Persons’ index of trade, could be largely attributed to the rate of change in the level of prices. In his conclusion, Fisher noted that “the so-called ‘business cycle’… seem[s] to be largely mythical.”62 In the decade preceding the Depression, one of America’s leading economists increasingly started viewing business cycles as a monetary phenomena. The Depression finally crystalized Fisher’s views on the causes of economic downturns, and he became one of the first modern monetarists.

Advertisement

In 1932, Fisher published Booms and Depression. The book introduced a theory of economic cycles called debt deflation, a theory that pins the roots of economic downturn to deflating levels of debt. The following year, Fisher expanded his theory and summarized his theory’s chain of events for readers:

Assuming a state of over-indebtedness exists, this will tend to liquidation through the alarm either of debtors or creditors or both… (1) Debt liquidation leads to distress selling and to (2) Contraction of deposit currency… This contraction of deposits and of their velocity, precipitated by distress selling, causes (3) A fall in the level of prices… Assuming, as above stated, that this fall of prices is not interfered with by reflation or otherwise, there must be (4) A still greater fall in the net worths of business, precipitating bankruptcies and (5) A like fall in profits, which in a "capitalistic," that is, a private-profit society, leads the concerns which are running at a loss to make (6) A reduction in output, in trade and in employment of labor. These losses, bankruptcies, and unemployment, lead to (7) Pessimism and loss of confidence, which in turn lead to (8) Hoarding and slowing down still more the velocity of circulation. The above eight changes cause (9) Complicated disturbances in the rates of interest, in particular, a fall in the nominal, or money, rates and a rise in the real, or commodity, rates of interest.63

In the book, Fisher included a twenty-one page chapter that outlined remedial policy, mainly monetary, to be taken during downturns. As the final remedial step “needed only in emergencies,” Fisher listed “stimulating borrowers and buyers” through “stamped dollar” subsidies that lost value over time.64 Throughout the New Deal, Fisher maintained that private industry subsidies were preferable to the “slow, clumsy, inefficient and costly” government-led public work programs.65

Fisher’s research and beliefs led him to energetically lobby for public policies during the Depression and the Recession. From 1933 to 1939, he wrote more than one hundred letters to President Roosevelt.66 Although overshadowed by Keynes and somewhat sidelined by the President, Fisher continued pressing for the adoption of his remedies. These solutions, however, all but excluded fiscal policy measures; his roots in laissez-faire thought started showing. In a 1934 response to the price setting measures of the Agricultural Adjustment Act (1933) and the National Recovery Administration (1933), Fisher informed the President of his objection to “the philosophy of wealth destruction and limitation as a means of enhancing the money values for certain classes at the expense of the nation as a whole.” He pointedly added, “On this matter some of the ‘brains trust’ do not seem to have brains to trust.”67

On the brink of the Recession and after successful Depression recovery efforts, Fisher again wrote to the President on October 24, 1937 to argue “it was not government expenditure which pulled us out of the depression… [but rather the expansion of] check-book money which turned over twenty times a year.”68 The full onset of the Recession brought Fisher a feeling of personal failure. In a letter to his wife on December 12, 1937, Fisher said, “I’m going to make a desperate effort to stick a pin in F.D.R.” In the same letter, he also reflected on his inability to sway Roosevelt: “Why couldn’t I have influenced the President more and earlier! I suppose it’s my shortcoming.”69

That same month, Fisher wrote to Marriner Eccles, the Chairman of the Board of Governors of the Federal Reserve System, and presented his views on the Recession. His first point declared that “this ‘recession’ is very largely monetary,” while in his second point, he agreed with Eccles’ view that “the ‘monopoly’ price of labor is largely responsible for unemployment.”70 71 As will be later discussed, some economists have considered this wage increase, brought about by the Supreme Court’s upholding of the 1935 National Labor Relations Act, one of the more minor causes of the Recession. However, it is overwhelmingly rejected as a contributing factor.Continued on Next Page »